I used to think “German company” was an easy phrase.

German name. German factory. German workers. German future.

Simple, right?

But after living in Germany and looking at the job market more seriously, I started to feel that this is not so simple anymore. You see Bosch, Mercedes-Benz, BMW, Volkswagen, Siemens, SAP, Lidl, Aldi, Schwarz IT, and all these names that sound very German. Then you read news about layoffs, energy cost, the nuclear phase-out, Chinese companies, American investors, AI acquisitions, private equity, foreign ownership, immigration, Ausbildung, startup bureaucracy, and suddenly the question becomes a bit uncomfortable.

Who actually owns “Made in Germany” now?

And maybe more important for students like us: if we want to work in Germany, should we only care about the brand name on the job ad? Or should we also understand who owns the company, who controls the money, and where the future jobs will be?

This article started from a YouTube video about German industry being in trouble. But I do not want this article to be only a reaction to one dramatic video. I want to use it as a trigger, then ask a more useful question.

Not “Is Germany dead?”

That is too dramatic. Also, honestly, I do not think it is helpful.

At first, I thought this article was only about who owns German companies. But after adding more research, I think the real question became wider:

When people say “German industry”, how much of the brand, workforce, factories, energy policy, founder system, capital, and decision power is actually German today?

And because this topic has a lot of finance, policy, and energy words, I will explain it like I would explain it to a classmate. We will use a pho shop, a banh mi shop, a nail shop, a kebab shop, and maybe a German bakery before we talk about DAX companies, nuclear power, company formation, and foreign direct investment.

If you can understand who controls a family restaurant, you can understand the basic logic of company ownership.

TL;DR

Germany is not “dead.” But the old image of German industry is becoming more complicated.

A company can still have a German name, German workers, German factories, and German engineering, while some of the capital and decision power comes from outside Germany. This is normal for many large listed companies. EY’s 2025 DAX analysis, for example, said foreign institutional investors held 52.6 percent of identified DAX shareholder capital, while German institutional investors held 33.1 percent [R1].

The Mittelstand is still extremely important. IfM Bonn reported 3.443 million SMEs in Germany in 2023, with 19.1 million employees subject to social insurance and 1.2 million trainees [R2]. So yes, the “real German economy” is not only BMW and Mercedes-Benz. It is also thousands of specialized companies that many students never hear about.

But pressure is real. Energy cost, the nuclear exit, succession, financing, export weakness, automotive transition, bureaucracy, and global competition make some companies more open to outside capital. Foreign investment is not automatically bad. Sometimes it saves jobs. Sometimes it keeps a factory alive. But it can also move important decisions away from Germany.

The article now has five connected layers: who owns famous brands, how Germany protects strategic companies compared with China, how migration and Ausbildung feed the workforce, why heavy paperwork can make buying old companies easier than starting new ones, and why China, Germany, and the United States are entering the AI and demographic race from very different positions.

For students, the lesson is simple: do not apply only because the logo is famous. Ask where the growth is. Ask whether the company is investing in the future. Ask whether energy, software, automation, process improvement, and new-product work are still happening in Germany. Also ask one harder question: is this country still creating future work, or only protecting old work?

Before Germany, Let’s Talk About A Pho Shop

Okay, let me back up a bit.

Imagine your family owns a pho shop in Ho Chi Minh City.

The shop is famous in the neighborhood. Your auntie cooks the broth. Your uncle buys the beef. Your cousin handles GrabFood orders. The sign outside still has your family name. Everyone says, “This is a Vietnamese family business.”

Then rent goes up. Beef gets more expensive. Electricity gets more expensive. The shop needs a new kitchen, but the family does not have enough money.

One investor comes in and says:

“I will pay for 60 percent of the business. The shop can keep the name. Your auntie can still cook. The staff can stay. But for big decisions, like opening another branch or changing the menu, I need a say.”

So what is the shop now?

Is it still a family pho shop?

Yes, in one way.

Is it fully controlled by the family?

No, not anymore.

This is the first key idea. Brand and control are not the same thing.

Now change the pho shop to a kebab shop in Heilbronn. Same logic. The name outside can stay local. The people working inside can stay local. The food can still taste the same. But if an outside investor owns most of the business, the biggest decisions may no longer come only from the original owner.

That is company ownership in simple language.

When we talk about German companies, the same logic applies. The logo can be German. The workers can be German. The factory can be in Baden-Wurttemberg. But the owners, shareholders, and future investment decisions can be global.

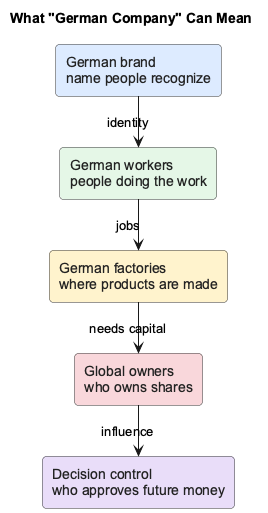

The First Diagram: What “German Company” Can Mean

I want to keep the diagrams simple because the YouTube summary diagrams were useful, but they were a bit too heavy for normal readers. For this article, one diagram should answer one question only.

This is the whole article in one picture.

“German company” can mean many layers:

| Layer | Simple meaning | Student question |

|---|---|---|

| Brand | The name people recognize | Is the logo famous? |

| Workers | People doing the work | Are jobs still in Germany? |

| Factory | Where things are made | Is production still here? |

| Owners | Who owns shares or capital | Who benefits if the company wins? |

| Control | Who approves future decisions | Who decides hiring, closing, investing? |

When all five layers are German, the story is simple.

But in the real world, those layers can split.

And this is where many students get confused. We look at the brand first because the brand is visible. But ownership and control are often hidden inside annual reports, shareholder structures, family offices, investment funds, or holding companies.

Big German Brands Often Have Global Money Behind Them

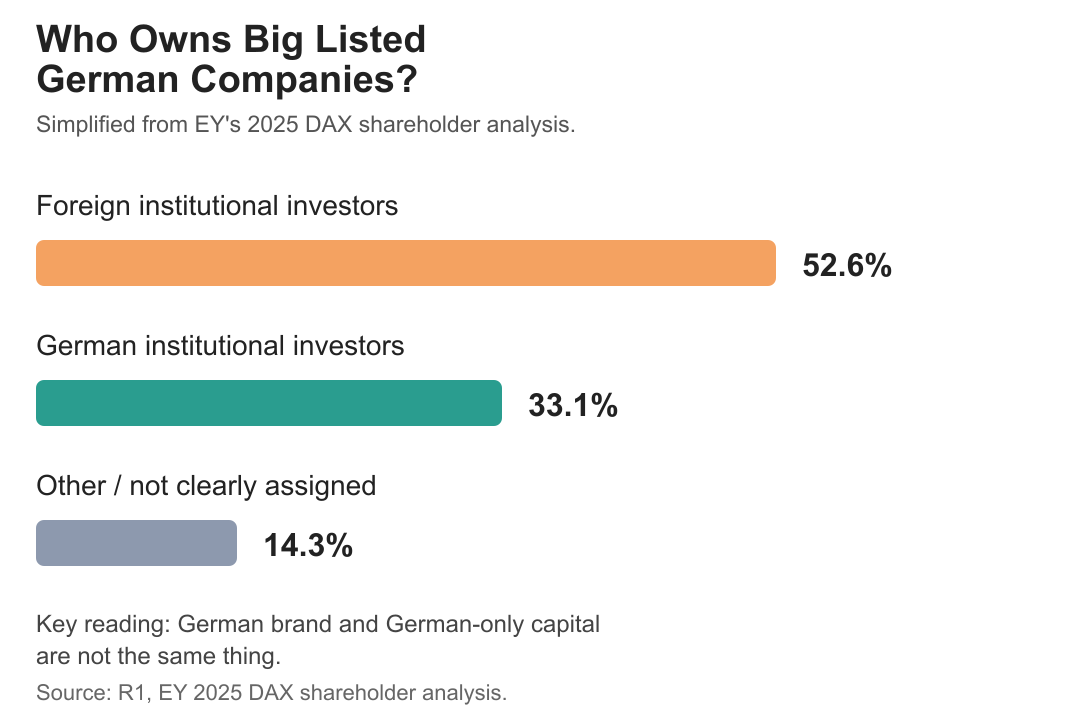

Let’s start with large listed companies.

If a company is listed on the stock market, people and institutions around the world can buy pieces of it. A pension fund in Canada can own shares. A US asset manager can own shares. A German insurance company can own shares. A private investor in Vietnam can own shares through an app.

This does not mean the company is fake German.

It means the company is part of global capital markets.

Here is the simple chart from EY’s 2025 DAX ownership analysis:

EY reported that foreign institutional investors held 52.6 percent of identified DAX shareholder capital in its 2025 analysis. German institutional investors held 33.1 percent [R1].

Let’s translate that into banh mi language.

Imagine a famous banh mi shop in Saigon becomes huge and opens many branches. It still has the original recipe. It still hires Vietnamese workers. It still has Vietnamese customers. But to expand, it sells shares. Now investors from Singapore, Japan, Germany, and the US own pieces of it.

Is it still a Vietnamese brand?

Yes.

Is all the money Vietnamese?

No.

Is that automatically bad?

Not always.

Outside capital can help a company grow faster. It can fund new factories, software systems, research, hiring, and international expansion. But it also means the company must answer to owners who may care about return, dividend, share price, or strategy from a global perspective.

For a student, this matters because a famous brand does not automatically mean stable local hiring. A company may still be famous but under pressure from shareholders to cut cost. Or it may be globally owned but still investing heavily in Germany. We need to look deeper.

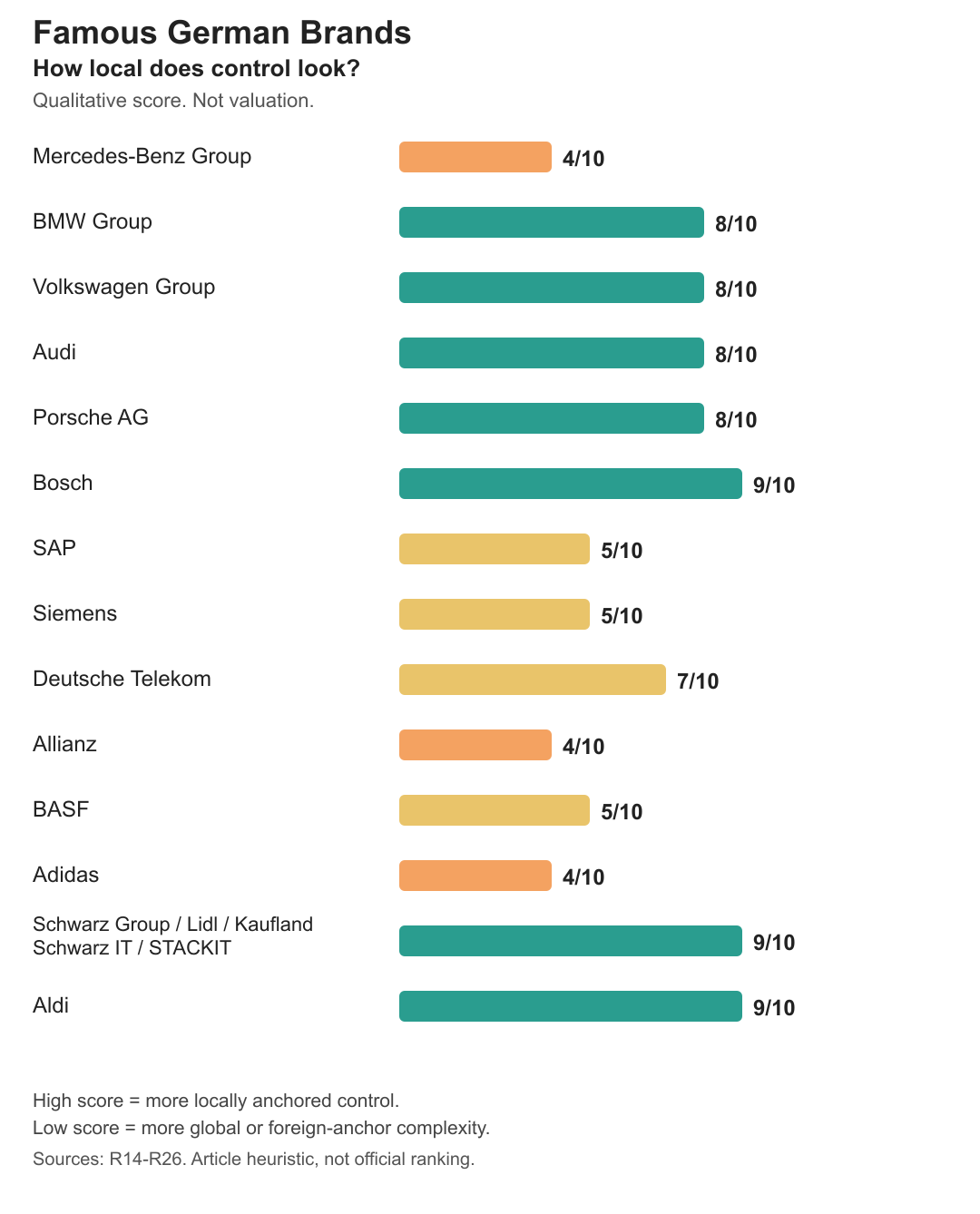

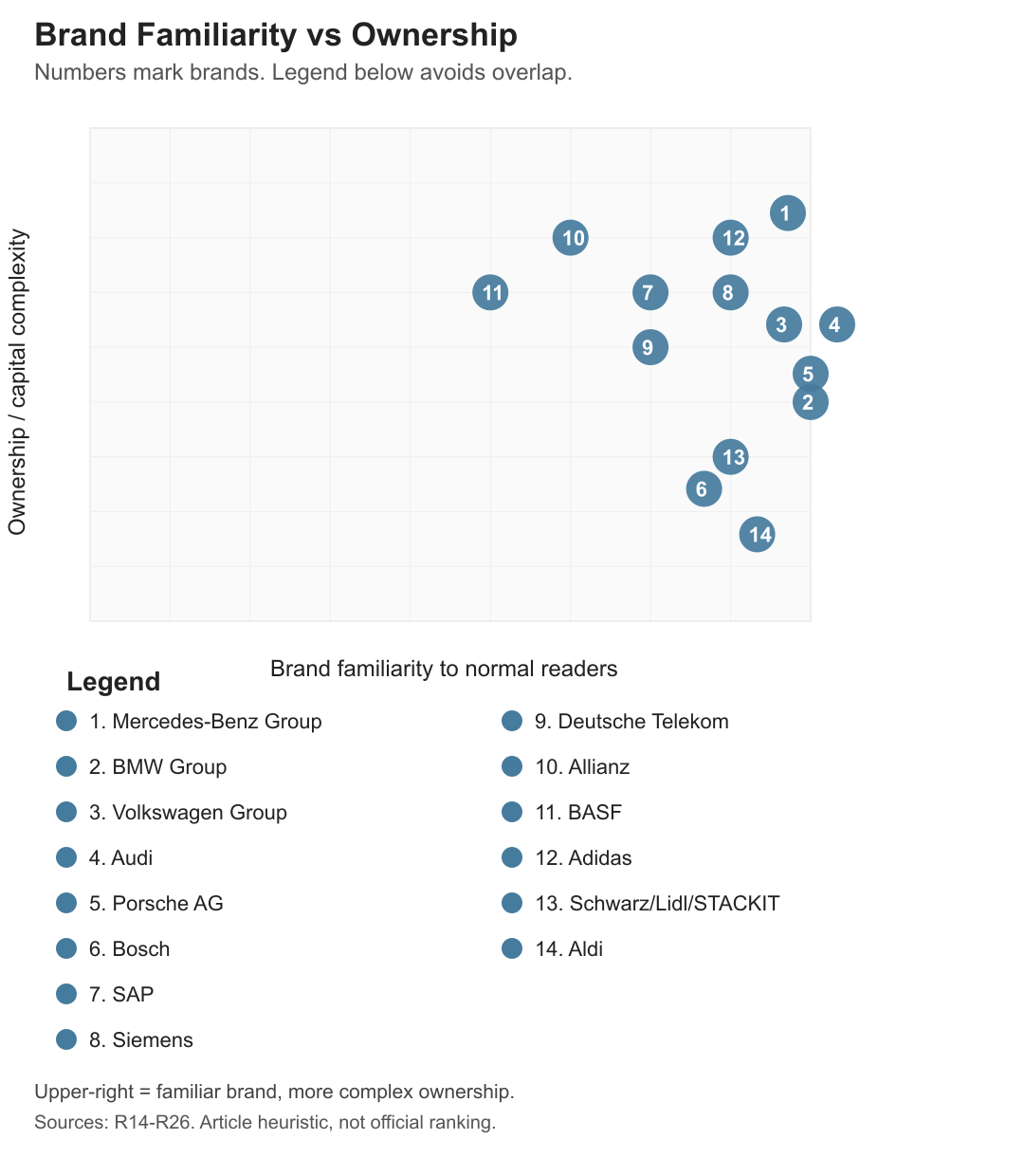

Famous Brands: The Logos We Actually Know

DAX, Mittelstand, and foreign capital can sound abstract, but normal readers do not wake up in the morning thinking about “institutional shareholder structure.” We think about Mercedes-Benz, BMW, Audi, Porsche, Bosch, SAP, Siemens, Adidas, Lidl, Aldi, and maybe Deutsche Telekom because our phone contract is expensive again.

Here is the more useful brand map.

This chart is not a stock-market ranking. It is a student-reading score. High score means the disclosed ownership/control pattern looks more locally anchored. Low score means the brand has more global/free-float/foreign-anchor complexity.

How did I build this score? I combined official shareholder or ownership pages and public company profiles in the reference list from R14 to R26. I gave higher scores to companies with clear German family, foundation, state, or group-control anchors, and lower scores to companies with high free float, global institutional ownership, or foreign strategic anchors. This is why Bosch, Aldi, and Schwarz Group score high, while Allianz, Adidas, and Mercedes-Benz look more globally complex. It is a reading tool, not an official ownership index.

Some examples:

- Mercedes-Benz is a German icon, but its shareholder structure includes major foreign anchor shareholders such as BAIC and Li Shufu, plus other institutional investors [R14].

- BMW still has a strong German family anchor through Stefan Quandt and Susanne Klatten, while also having a large free float [R15].

- Volkswagen is complicated but still strongly anchored through Porsche SE and Lower Saxony voting rights, with Qatar also important [R16].

- Audi is not a separate ownership story in the same way because it sits inside the Volkswagen Group [R16].

- Porsche AG is also tied to the Volkswagen/Porsche SE structure, with ordinary and preferred-share layers that normal people almost never think about when they see a 911 on the street [R17].

- Bosch is very different from a listed company. Its structure is tied to the Robert Bosch Stiftung and a trust structure, which means it is not controlled like a normal stock-market company [R18].

- SAP is German by origin and headquarters, but its free float is high, so global capital-market logic matters [R19].

- Deutsche Telekom still has German state/KfW anchors, but institutional investors are also a major part of the ownership picture [R21].

- Allianz, BASF, Adidas, and Siemens are global listed-company stories, not simple local-family-company stories [R20], [R22], [R23], [R24].

- Schwarz Group, Lidl, Kaufland, Schwarz IT, and STACKIT are important because this is not only supermarket retail anymore. Schwarz IT and STACKIT show how a German retail empire is also building serious digital and cloud infrastructure [R25].

- Aldi is famous and privately held, but public shareholder transparency is limited compared with listed companies [R26].

Now look at this scatter map.

The upper-right area means: “Everyone knows the brand, but ownership/control is not simple.”

For this scatter chart, the x-axis is my normal-reader brand familiarity estimate, while the y-axis uses the same ownership-complexity logic from the brand-control table. I numbered the brands because direct labels were overlapping and hard to read. So if someone wants to challenge the chart, the right thing to challenge is the scoring assumption, not the raw company facts. The raw facts come from the source pages listed in R14 to R26.

This is why brand names can trick students.

You see Mercedes-Benz and think “German company.” That is true, but incomplete. You see Lidl and think “supermarket.” That is true, but incomplete, because Schwarz Group also has Schwarz IT and STACKIT. You see SAP and think “German software.” True, but if the company is mostly free float, then global investors matter.

So maybe the better question is not “Is this German?”

The better question is:

Which part of this company is still rooted in Germany, and which part is already global?

That question is more useful than national pride. It is also more useful for job search.

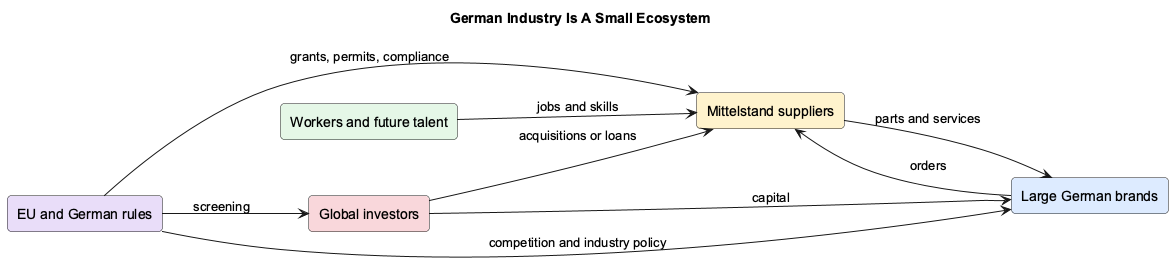

Mittelstand: The Real Germany Many Students Do Not See

When foreigners talk about German industry, we often talk about BMW, Mercedes-Benz, Volkswagen, Bosch, Siemens, SAP, and other famous names.

But the German economy is not only the big names.

Germany has a huge layer called the Mittelstand.

Simple meaning: Mittelstand means small and medium-sized companies, often family-owned, often specialized, and often very important in one narrow product area.

Vietnam example: imagine a family company in Binh Duong that only makes one type of metal part for furniture factories. Normal people do not know the brand. But many factories depend on it.

Germany example: imagine a company in a small town that makes one special sensor, machine tool, valve, screw, packaging machine, or industrial component. It may not be famous on TikTok. But global factories may need it.

IfM Bonn reported 3.443 million SMEs in Germany in 2023. These SMEs employed 19.1 million people subject to social insurance and trained 1.2 million trainees [R2]. That is why people say the Mittelstand is the backbone of Germany.

But “backbone” does not mean “cannot get tired.”

KfW’s 2025 SME Panel is based on 9,495 SMEs and describes a sector dealing with difficult conditions, weak sentiment, and pressure around investment [R3]. The details matter, but the simple student version is this:

| Pressure | Pho shop version | German company version | Why students should care |

|---|---|---|---|

| Energy cost | Electricity for the kitchen gets expensive | Factory power and gas costs rise | Less money for hiring |

| Succession | Children do not want to run the shop | Family owner has no successor | Company may sell or close |

| Investment need | Need a new oven or delivery system | Need robots, software, EV equipment | Future jobs depend on upgrades |

| Customer pressure | Big delivery app takes margin | Big OEM pushes supplier prices down | Suppliers cut costs first |

| Export weakness | Fewer tourists buy food | Foreign customers order less | Hiring slows in export regions |

This is why I think students should not only search for big brands. Some Mittelstand companies can offer better learning, more responsibility, and real future work. But we also need to check whether the company is investing or just surviving.

When Outside Money Arrives, It Is Not Always A Villain Story

Here is where the topic becomes sensitive.

When people hear “foreign acquisition,” they may immediately think, “Oh no, another country is buying Germany.”

But let’s slow down.

Sometimes outside money arrives because a company is strong and wants to grow. Sometimes it arrives because the company is weak and needs help. Sometimes it is normal portfolio investment. Sometimes it is strategic, because the buyer wants technology, market access, brand trust, or production inside Europe.

This is why I do not want to write a simple anti-China or anti-foreign-investor article. That would be easy, but not honest.

Foreign capital can do good things:

- keep a factory alive

- protect jobs in the short term

- fund new machines

- help a brand enter new markets

- connect the company to a larger supply chain

But it can also create risks:

- future research may move elsewhere

- board decisions may change

- local suppliers may lose influence

- workers may keep jobs today but lose future bargaining power

- Germany may keep the brand but lose some strategic control

This is why the EU has foreign direct investment screening rules. The European Commission says screening is used to protect security and public order, and in 2025 it welcomed a political agreement on a strengthened EU foreign direct investment screening system [R5], [R6]. That does not mean Europe wants to block all foreign investment. It means ownership is now also a policy question, not only a finance question.

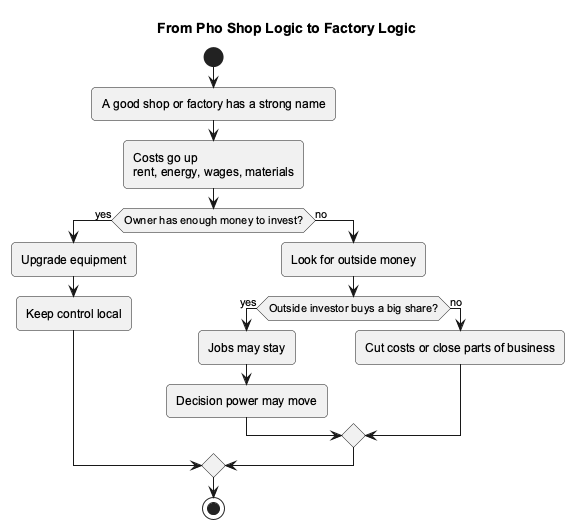

The Pho Shop To Factory Flow

This is the simple version of the acquisition pattern.

I like this diagram because it avoids drama.

It does not say “foreign investor bad.”

It says: when costs go up and the owner cannot invest alone, outside money becomes more attractive.

That is true for a pho shop. It is true for a kebab shop. It can also be true for a German supplier factory.

Selected Case Studies: The Pattern Is Real, But Different Each Time

Here are a few examples that help explain the pattern.

| Case | Sector | What happened | Simple meaning |

|---|---|---|---|

| Geely and Volvo Cars | Automotive | Geely completed the purchase of Volvo Cars from Ford in 2010 [R8] | A Chinese car group bought a European brand and used it as a long-term platform |

| ChemChina and Pirelli | Tires and industrial technology | Pirelli announced board advisory steps around the Camfin-ChemChina tender offer in 2015 [R9] | A European industrial brand became part of a Chinese-linked transaction debate |

| Midea and KUKA | Robotics | Midea made a takeover offer for German robotics company KUKA in 2016 [R7] | A German automation champion became a major foreign-acquisition debate |

| Chery in Spain | Automotive production | Eurofound recorded Ebro’s business expansion linked to Chery and the former Nissan Barcelona plant [R10] | Chinese carmakers are not only exporting to Europe, they are also localizing production |

These cases are not identical.

Volvo is not KUKA. KUKA is not Pirelli. Spain is not Germany.

But they show one repeated question:

When outside money enters, what stays local and what moves?

Does the brand stay?

Do the workers stay?

Does research stay?

Does decision power stay?

Does the future investment stay?

This is the part a normal job seeker rarely sees from the outside.

But Wait, Does China Allow The Same Thing Back?

This is the uncomfortable question.

If Chinese companies can buy European brands, robotics companies, tire companies, supplier assets, or factories, can an American or European buyer do the same thing to a sensitive Chinese AI company?

Recently, this question became very real.

In April 2026, TechCrunch reported that Chinese regulators blocked or moved to unwind Meta’s reported acquisition of Manus AI, an agentic AI company with Chinese origins [R35]. I am wording this carefully because this is a current-news case and the full legal details are not as transparent as a normal listed-company annual report. But the signal is important.

The signal is not only “China blocked one deal.”

The bigger signal is:

China is willing to treat AI company control as a national strategic issue.

Imagine the pho shop example again, but now the recipe is not only soup. The recipe is an AI system that can automate office work, agent workflows, and maybe future productivity. If an outside buyer wants to buy it, the government may say: “Wait, this is not only a private business deal. This is strategic capability.”

That is a very different mindset from a purely open market.

China Has A Stronger Protection Toolbox

China is not closed to all foreign money. This is important. Foreign investors can access Chinese securities through regulated channels, and China has also opened some manufacturing access over time [R38], [R39].

But buying shares is not the same as controlling a strategic company.

That is the key difference.

A foreign investor may be able to buy some stock exposure to Chinese companies. But if the deal touches sensitive technology, data, national security, media, internet platforms, AI, infrastructure, or another strategic area, China has stronger state tools to review, restrict, or stop it. China has foreign investment security review measures [R37]. It has sector access controls through negative lists and related policy tools [R38]. It also has technology export-control mechanisms for sensitive technologies [R40].

Germany and the EU also screen foreign investment. The European Commission’s FDI screening framework exists, and the EU has been moving to strengthen it [R5], [R6]. So it would be wrong to say Europe has no protection.

But the style is different.

China’s model is more state-directed. Germany and the EU are more legalistic, procedural, and slower.

Here is a simple comparison.

For normal readers, I would summarize it like this:

| Question | China-style answer | Germany/EU-style answer |

|---|---|---|

| Can foreigners invest? | Yes, but through controlled doors | Yes, especially in listed markets |

| Can foreigners buy any company they want? | No, strategic sectors can be blocked | No, but screening is narrower and more procedural |

| Is technology treated as national power? | Very clearly yes | Increasingly yes, but with more debate |

| Can the state move quickly? | Often yes | Often slower |

| Is this more open-market friendly? | Less | More |

| Is this more protective? | Often yes | Sometimes, but uneven |

So is China “better” at protecting companies?

It depends what you mean by better.

If “better” means protecting strategic control, China is probably stronger.

If “better” means keeping markets open, predictable, and investor-friendly, Germany/EU may look better.

If “better” means protecting workers and future innovation at the same time, then the answer is more complicated.

China can stop control from leaving. But strong state control can also scare investors, reduce trust, and make private entrepreneurs worry about political risk. Germany/EU can attract global capital more easily, but that openness can also allow slow bleeding of ownership, technology, and decision power if screening comes too late.

This is the tradeoff.

Open markets bring money.

Strong protection keeps control.

The hard part is designing a system that keeps both enough money and enough control.

What Germany Might Learn Without Copying China

I do not think Germany should simply copy China’s system. The political systems are different. The legal culture is different. The EU single market is different. German companies also benefit from being trusted by international investors.

But Germany can still learn one thing:

Strategic capability should be identified before the company is distressed, not after it is already cheap.

This is where I think Germany and Europe can improve.

If a company is important for robotics, industrial software, AI, grid infrastructure, semiconductor equipment, healthcare technology, defense supply chains, or energy systems, then the country should not wait until the company is weak and then suddenly panic about foreign acquisition.

That is like ignoring your family pho shop for ten years, then crying when someone buys it because rent became too high.

Protecting a company does not only mean blocking the buyer at the last minute.

It can mean:

- helping strategic companies access patient capital earlier

- supporting succession for Mittelstand owners

- reducing energy and permitting pressure

- helping companies upgrade technology before they become distressed

- keeping research and development in Germany

- building European buyers and funds that can compete with foreign buyers

- making screening rules clear before deals happen

For students, this matters because the future job market depends on where the future work stays.

If Germany keeps the factory but loses the software, the AI, the patents, the board decisions, and the new investment, then the job market becomes thinner for young people.

If Germany protects only the brand but not the capability, then “Made in Germany” becomes a label, not a strategy.

The Startup Problem: If Opening A New Company Is Too Hard, Buying An Old One Becomes Attractive

There is another part of this ownership story that I missed at first.

It is not only about who buys German companies.

It is also about why people may prefer to buy an existing German company instead of starting a new one.

If you are a foreign student, a migrant founder, or even a local German person with a business idea, Germany can feel heavy. Not impossible, but heavy. There is notary work. There is the commercial register. There are tax numbers. There is the bank account issue. There is German-language paperwork. There are permits. There are local offices. There is the feeling that every step has another form behind it.

KfW’s 2025 Entrepreneurship Monitor gives the broader founder-activity context for Germany, while OECD country notes point to inclusion and ecosystem challenges around entrepreneurship in Germany [R41], [R44]. The German Startup Monitor 2025 also shows the ecosystem still wrestling with capital, partnerships, and founder conditions [R45]. Germany does have founder-support programs, including EXIST and official guidance for starting a business [R42], [R43]. So it is not that Germany does nothing.

But the lived experience still matters.

If opening a new company feels like climbing a mountain, then buying an old company can feel like taking over a house that already has electricity, water, address registration, customers, a tax file, and a working door key.

That is a very important insight.

For a foreign investor, buying an existing German company may be easier than starting from zero because the old company already has:

- a legal entity

- bank accounts

- commercial register entry

- tax history

- supplier contracts

- customer relationships

- permits

- trained workers

- local credibility

- German-language administrative memory

In Vietnam terms, imagine opening a new restaurant from zero versus buying an existing pho shop that already has customers, kitchen approval, GrabFood reviews, staff, and a known location. Even if the shop is old and tired, it may still be easier than starting from an empty room.

In Germany terms, imagine starting a new small manufacturing company versus buying a small Mittelstand supplier that already has machines, certification, workers, supplier codes, customer audits, and tax history. Suddenly, the old company becomes valuable not only because of profit, but because the paperwork has already been survived.

That is why bureaucracy can accidentally protect old companies and punish new ones.

At first, that sounds good for old companies.

But long term? I am not sure it is good for Germany.

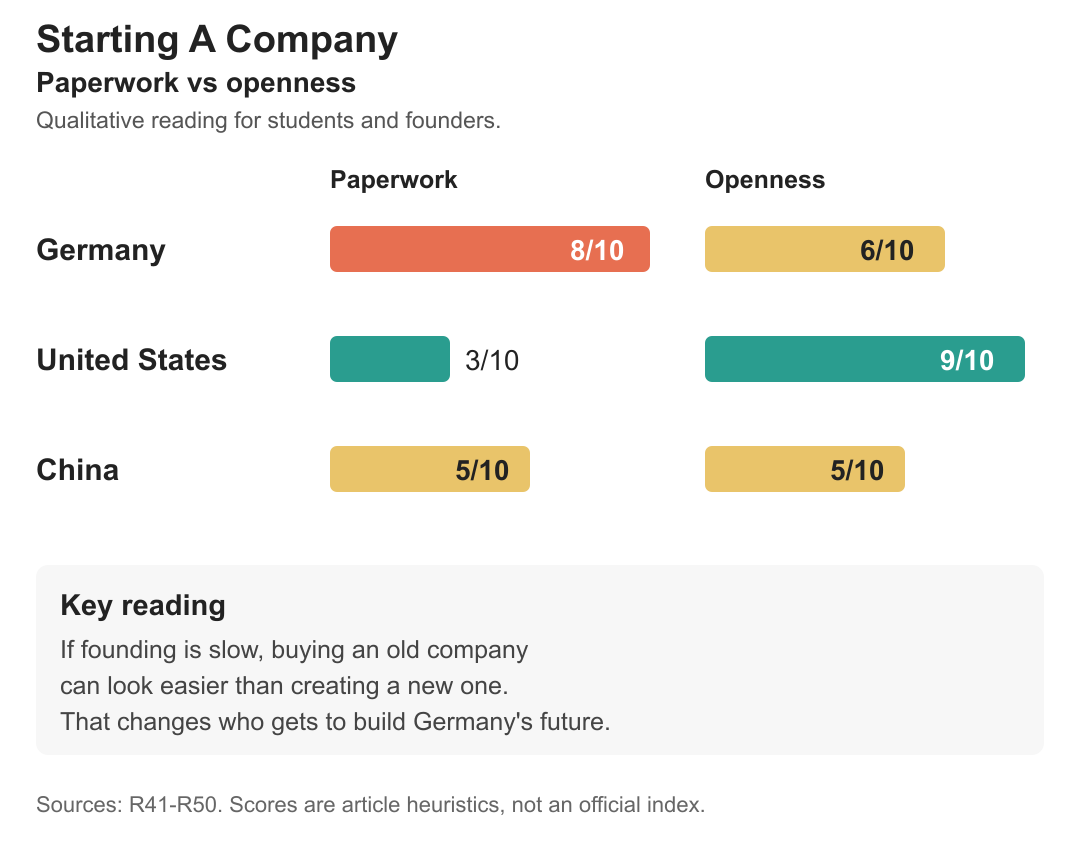

Germany, USA, China: Three Different Founder Experiences

Here is a simple comparison.

For this chart, the scores are qualitative. I used KfW, OECD, Startup Verband, German official founder guidance, US company-formation sources, and Chinese official business-registration guidance [R41]-[R50]. The chart does not say “Germany is impossible” or “the US is perfect.” It says the mechanical act of opening a company feels much lighter in the US than in Germany, while China can streamline registration but still keeps stronger state control over strategic sectors.

The United States is not perfect. Immigration is hard. Visa and work authorization can be brutal. But mechanically opening an LLC or corporation is often much easier. Delaware, for example, has standardized corporate services and processing options [R46]. Tools like Stripe Atlas also show how international founders can form a US company remotely, even though immigration and banking are still separate problems [R47]. The US Small Business Administration explains business structures like LLCs in a very modular way [R48].

China is different again. It is not simply “easy” or “open.” For foreign-invested companies, China has formal registration processes, and official Chinese portals provide business-entry and enterprise-registration guidance [R49], [R50]. But as we discussed earlier, China is still much more state-directed around strategic sectors, market access, and technology control [R37], [R38], [R40].

Germany sits in a strange middle.

It wants innovation. It wants skilled migrants. It wants startups. It wants international students to stay. It wants digitalization.

But the paperwork culture often sends a different message:

You are welcome, but please bring patience, German language, a folder of documents, and emotional stability.

I am joking, but only half joking.

For a Vietnamese student, this matters. If you study in the US, you may feel that opening a small LLC is a normal weekend project. If you study in Germany, you may feel that opening a business is a full administrative life event. If you study in China, you may see a system that can move fast when the state wants it to move fast, but also a system where strategic control is never fully just private.

Why This Changes The Ownership Story

This startup-friction problem fits directly into the “Who owns Germany?” question.

If it is hard to create new German companies, then Germany depends more on old companies.

If Germany depends more on old companies, then old companies become acquisition targets.

If old companies become acquisition targets, then foreign buyers with patient capital can enter more easily.

If foreign buyers enter more easily than new founders, then the economy slowly tilts toward ownership transfer instead of company creation.

That is the danger.

It is not only “Chinese companies buy German companies.”

It is also:

German bureaucracy makes new company creation harder, so existing companies become the easiest doorway into the German market.

This is why paperwork is not boring.

Paperwork shapes ownership.

Paperwork shapes who can start.

Paperwork shapes whether a student becomes an employee only, or also a founder.

Paperwork shapes whether the next Bosch, SAP, or Schwarz IT can be born in Germany, or whether Germany mostly keeps defending the old champions.

What Germany Should Do Better

I do not think the answer is “remove all regulation.” That would be too naive.

Germany has rules for good reasons: worker protection, tax compliance, safety, consumer trust, data protection, environmental rules, and fair competition. These things matter.

But Germany needs to separate useful protection from administrative friction.

Useful protection means:

- stop strategic technology from being sold too easily

- protect workers from abusive employers

- keep tax and safety rules fair

- screen sensitive acquisitions earlier

- support Mittelstand succession before crisis

Administrative friction means:

- duplicate forms

- slow register processes

- unclear office responsibility

- German-only instructions for international founders

- bank account barriers before company operations

- paperwork that protects nobody but delays everyone

If Germany wants more new companies, especially from international students and skilled migrants, it should make the first 90 days of founding much easier:

- one digital founder portal in English and German

- clear student-founder rules for residence permits

- fast tax number issuance

- founder-friendly bank onboarding

- simple templates for small service businesses

- startup visa and post-study founder pathways that normal students can understand

- local city-level startup desks that speak practical English

- lower notary/register friction for small digital businesses

Because if Germany does not make new company creation easier, then the future may look like this:

- old companies carry the economy

- old companies become expensive to modernize

- founders avoid Germany or stay employees

- foreign buyers buy existing companies

- Germany keeps the brand but loses more control

That is not collapse.

But it is slow ownership drift.

And honestly, that may be more dangerous than one dramatic crisis.

Timeline: How The Old Model Became More Fragile

This is my simple timeline. It is not perfect, but it helps me organize the story.

Small honesty note: I could be wrong in some interpretations because ownership data is messy, and my sample size of case studies is small. So I treat this article as a useful map for students, not as a final economic model of Germany.

| Period | What changed | Simple student meaning |

|---|---|---|

| Before 2020 | Germany benefited from strong exports, strong engineering, and relatively stable industrial assumptions | The old model still looked solid |

| 2020-2021 | Covid disrupted supply chains | Companies learned that “global supply chain” can break |

| 2022 | Russia’s war against Ukraine changed the energy picture in Europe | Cheap-energy assumptions became weaker |

| 2023-2025 | Automotive transition, China competition, higher costs, and weak demand pressured suppliers | Some old jobs became less safe |

| 2025-2026 | Europe discusses stronger screening and industrial resilience | Ownership becomes a policy issue, not only a business issue |

This does not mean everything started in 2022. That would be too simple.

The EV transition was already coming. China was already moving from customer to competitor. German bureaucracy and permitting debates were already there. Mittelstand succession was already a topic. But the energy shock made many hidden weaknesses easier to see.

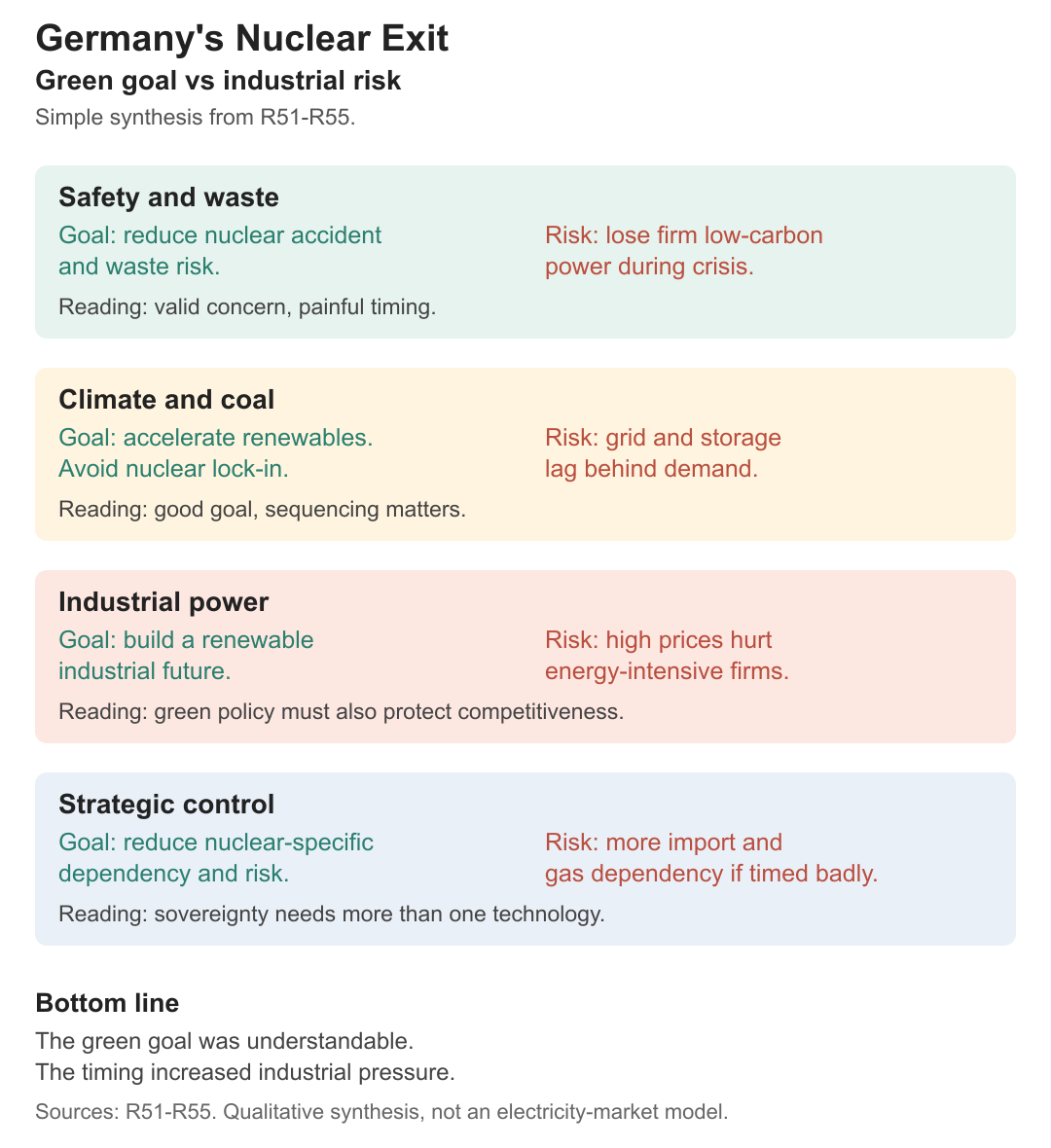

Nuclear, The Green Movement, And Industrial Reality

Now we need to talk about nuclear power.

This is a sensitive topic in Germany because it is not only an engineering question. It is also history, fear, environmental politics, public trust, and the Green movement.

Germany’s nuclear phase-out was not invented in one week. It came from a long anti-nuclear movement and a political decision path that became very hard to reverse. The Federal Office for the Safety of Nuclear Waste Management describes Germany’s nuclear phase-out and the final shutdown of the last reactors [R51]. During the 2022 energy crisis, Germany temporarily extended the life of the last three operating nuclear power plants, which shows that even policymakers knew the timing was difficult [R52].

Then on 15 April 2023, the last three reactors were shut down.

So was this good or bad?

My answer is: the Green movement had a valid concern, but the sequencing created industrial risk.

The valid concern is easy to understand. Nuclear has waste problems. Nuclear accidents are rare, but when they happen, people remember them for generations. Many Germans did not want that risk. From a democratic and environmental point of view, that feeling is real.

But the economic problem is also real.

If you remove firm low-carbon electricity before the renewable grid, storage, transmission, and industrial power-price system are ready, then energy-intensive companies feel more pressure. Germany wants green industry, but industry still needs affordable and reliable power. The IEA’s Germany 2025 review frames the energy transition as central to Germany’s competitiveness challenge [R54]. Agora’s 2025 energy-transition review also shows that the transition is not only about building renewables, but about making the whole system work [R55].

Fraunhofer ISE’s one-year review after the nuclear exit argued that renewable capacity expanded and fossil-fuel electricity fell significantly, so the story is not simply “nuclear closed, coal exploded forever” [R53]. That is important. We should not make lazy arguments.

But for this article, the ownership and job-market question is different:

Did the nuclear exit make Germany’s industrial base stronger at the exact moment when energy, China competition, and EV transition were already hurting it?

I think the answer is probably no.

This chart is not an electricity-market model. It combines five sources: the official phase-out timeline, the 2022 crisis extension context, Fraunhofer’s post-exit electricity-system review, the IEA 2025 Germany review, and Agora’s 2025 energy-transition review [R51], [R52], [R53], [R54], [R55].

The point is not “Green movement bad.”

The point is:

Green policy that ignores industrial timing can accidentally weaken the companies it wants to transform.

Think about the pho shop again. Imagine your family decides to stop using gas for cooking because electric cooking is cleaner. That may be a good long-term goal. But if the electric kitchen is not ready, electricity is expensive, and lunch customers still need food tomorrow, then the transition can hurt the shop before it becomes greener.

Germany’s energy transition has the same logic. The goal can be correct while the sequencing is painful.

For the future, Germany needs a greener economy, but it also needs industrial power that companies can afford. If not, green policy can push factories, capital, and future jobs away from Germany. Then Germany keeps the environmental intention, but loses some industrial capability.

That would be a bad trade.

Immigration: Germany Is Not Only German Labor Anymore

There is another layer we need to add.

Ownership is one side. Workforce is another side.

Germany still often asks for German language in job ads. Sometimes it feels like every posting says Deutschkenntnisse erforderlich, even when the company is globally owned, globally selling, or globally hiring. That is the strange feeling many international students have.

On paper, Germany wants skilled workers. In daily job ads, Germany still often wants German.

Both are true.

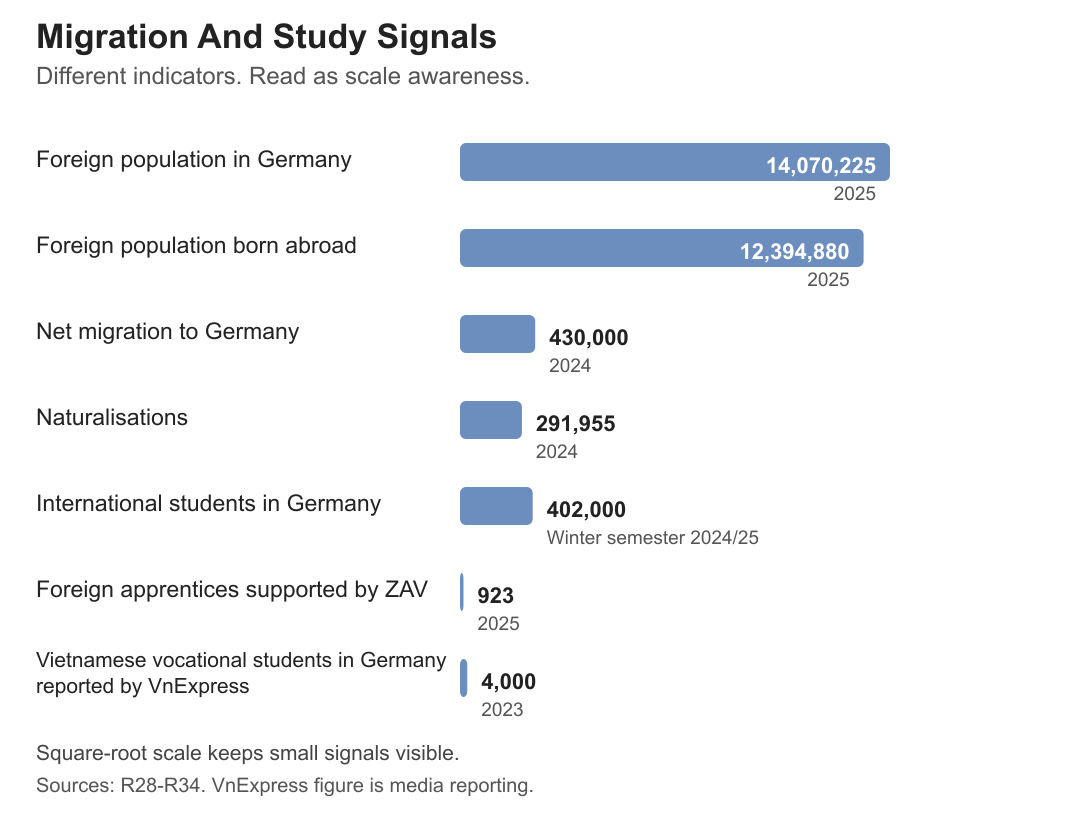

Destatis reported more than 14.07 million foreign nationals in Germany at the end of 2025 [R28]. It also reported 12.39 million foreign nationals born abroad [R29]. Net migration was 430,000 people in 2024 [R30]. Naturalisations reached 291,955 in 2024 [R31]. DAAD said Germany hosted more than 400,000 international students and doctoral candidates in winter semester 2024/25 [R32].

So no, modern Germany is not only “Germans working in German companies for German customers.” That is no longer the full picture.

This chart uses different indicators, so do not compare them like one normal bar chart. Foreign population, international students, naturalisations, and apprenticeships are different things. I made it mainly to show scale.

Germany is becoming more international in people, but still very German in language gatekeeping.

That is the contradiction.

Vietnamese Readers: The Ausbildung Path Is Real, But It Is Not The Whole Future

For Vietnamese readers, this part matters a lot.

Many Vietnamese people do not come to Germany through the same route as a master’s student in IT or business. A very common pathway is Ausbildung.

Simple meaning: Ausbildung is German vocational training. You learn at a workplace and a vocational school. It is not the same as university. It is closer to learning a profession while working.

Vietnamese version: imagine someone from Vietnam goes to Germany to train as a nurse, restaurant professional, hotel worker, mechanic, or other skilled worker. They are not only “studying abroad” in the university sense. They are entering the German labor system through a training contract.

German version: Ausbildung is one of Germany’s key workforce pipelines. It feeds hospitals, nursing homes, hotels, restaurants, workshops, logistics companies, and many technical trades.

The Bundesagentur für Arbeit said that in 2025, 923 young people from abroad started an apprenticeship in Germany with ZAV support, and Vietnam was among the countries named in that program context [R33]. I originally wanted to add a Vietnamese media figure here, but I removed it after URL checking because the link no longer resolved to the claimed article.

The bigger insight is still useful:

For Vietnamese migration to Germany, Ausbildung is not a side story. It is one of the main stories.

But here is my honest concern.

If Vietnamese people mostly enter Germany through nursing homes, restaurants, hotels, and low-to-mid wage vocational routes, while the ownership and strategic-control layer of German industry becomes more global, then Vietnamese workers may become part of the labor solution without being close to the decision layer.

That sounds harsh, but it is important.

Being needed is not the same as having power.

A nursing home may need Vietnamese workers. A restaurant may need Vietnamese trainees. A factory may need apprentices. But who designs the system? Who owns the company? Who controls wages? Who decides automation? Who decides whether software replaces admin work? Who decides whether the role has career growth?

This is why I think Vietnamese students should not only ask, “Can I get to Germany?”

They should also ask:

Which pathway gives me future bargaining power?

For some people, nursing Ausbildung is a good path. For some, hotel or restaurant Ausbildung may be practical. For others, university, IT, business analysis, data, automation, logistics, supply chain, or healthcare process work may create more long-term movement.

I am not saying one path is morally better. I am saying the paths lead to different rooms in the same German house.

Some rooms are close to decision-making. Some rooms are close to hard physical work. Some rooms are stable but capped. Some rooms are risky but higher-upside.

Students should know the difference before they choose.

China’s Pressure Is Different: Fewer Babies, Tired Youth, And No Immigration Cushion

Now we need to step outside Germany for a moment.

China looks powerful from the outside. It has manufacturing scale. It has huge supplier networks. It has fast infrastructure. It has strong state tools. It can protect a strategic AI company more aggressively than Germany or the EU would usually do. It can also buy foreign industrial assets when the deal passes the other country’s rules.

But China also has a different weakness.

Germany’s weakness is often bureaucracy, energy price, slow digitalization, and language gatekeeping. China’s weakness is more demographic and social.

The National Bureau of Statistics of China reported 9.54 million births and 10.93 million deaths in 2024 [R56]. So even though births improved a little from the previous year, the population still declined. Reuters, citing the official youth unemployment measure, reported that unemployment for urban people aged 16 to 24, excluding students, climbed to 18.9 percent in August 2025 [R57]. A youth development report also noted that China expected about 12.22 million university graduates in 2025 [R58].

Put that into normal language.

Imagine a huge pho restaurant chain. It has the best kitchen equipment, the strongest supply chain, and the government protects its secret recipe. But fewer young people want to become cooks, many graduates cannot find the job they studied for, and the older workers are ageing. The restaurant is still strong, but the people engine is under stress.

That is the China question.

China can protect ownership better than Germany. But can it keep enough young people motivated, employed, skilled, and willing to carry the next industrial cycle?

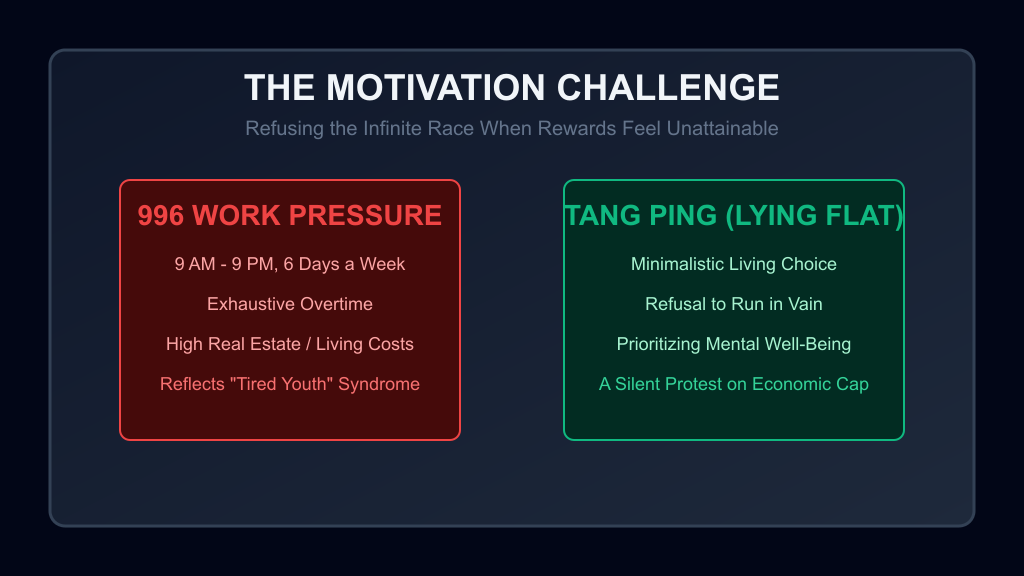

996, Tang Ping, And The Quiet Problem Of Motivation

This is where the terms 996 and tang ping appear.

996 means working from 9 a.m. to 9 p.m., six days per week. For a normal student, just read it as: work almost all the time. China has pushed back against excessive overtime legally through Supreme People’s Court and labor ministry case guidance, but the culture around long hours remains part of the discussion around technology and platform work [R64].

Tang ping means “lying flat.” It is not one official organization. It is more like a youth mood, a refusal to keep running forever when housing, work, competition, and family pressure feel too heavy. A 2026 PLOS ONE scoping review connects tang ping discussions with youth mental health, 996 pressure, and social stress among Chinese youth [R59].

This does not mean all Chinese young people are lazy. That would be a very bad and unfair reading.

The better reading is this:

When the reward of hard work feels too far away, young people start questioning the system.

Vietnamese readers can understand this easily. If your family tells you to study hard, get a degree, work in the city, buy a house, marry, support parents, and raise children, but the salary cannot catch the house price, then the old promise becomes weaker.

German readers can understand it too. If every job asks for experience, German language, certificates, internships, and perfect paperwork, but the salary after rent and tax feels tight, students also start asking: what exactly am I running toward?

Germany does not have tang ping in the same famous cultural form. But Germany has its own version of tiredness: long bureaucracy, slow hiring, expensive rent, language barriers, and young people wondering whether the system still gives them movement.

So this is not a China-only story.

It is a future-work story.

AI Talent: China Has Brains, The US Has Capital, Germany Has The Middle Path

AI makes the ownership story sharper.

If AI becomes the next productivity engine, then ownership is not only about factories. It is also about models, chips, data, cloud platforms, industrial software, patents, and the teams who know how to turn AI into daily work.

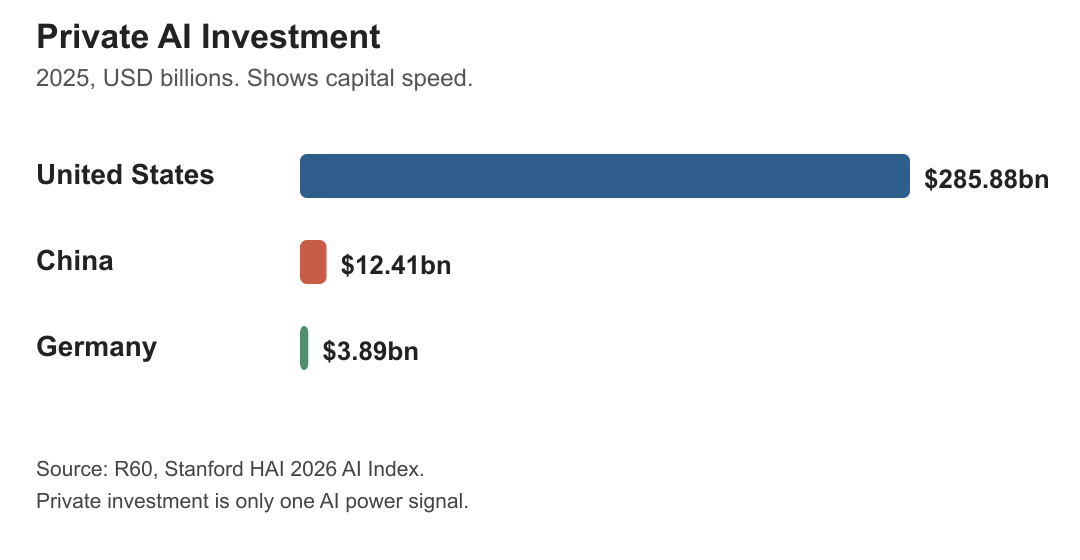

The Stanford HAI 2026 AI Index shows a very uneven private-investment picture. In 2025, the United States had about 285.88 billion US dollars in private AI investment, compared with about 12.41 billion for China and 3.89 billion for Germany [R60].

This chart is simple on purpose. It is not saying Americans are smarter, Chinese people are weak, or Germans cannot build AI. It is saying capital speed is very different.

If AI is like opening 1,000 new kitchens at the same time, the US has the investor money to buy ovens, hire chefs, test recipes, and throw away failed menus faster than everyone else. China has strong engineering depth, manufacturing scale, and state direction. Germany has excellent applied industry problems, but less AI capital and more slow process.

For Germany, the opportunity is not to copy Silicon Valley exactly. Germany’s chance is applied AI inside real industry:

- AI for factory quality control

- AI for energy management

- AI for logistics planning

- AI for SAP and ERP workflows

- AI for healthcare administration

- AI for industrial cybersecurity

- AI for engineering documentation

- AI for compliance and audit work

This is why I still think Germany can be interesting for international students.

Germany may not win the biggest foundation-model race. But Germany has many messy, expensive, real-world workflows where AI can save time. A student who understands both technology and German business process can become useful there.

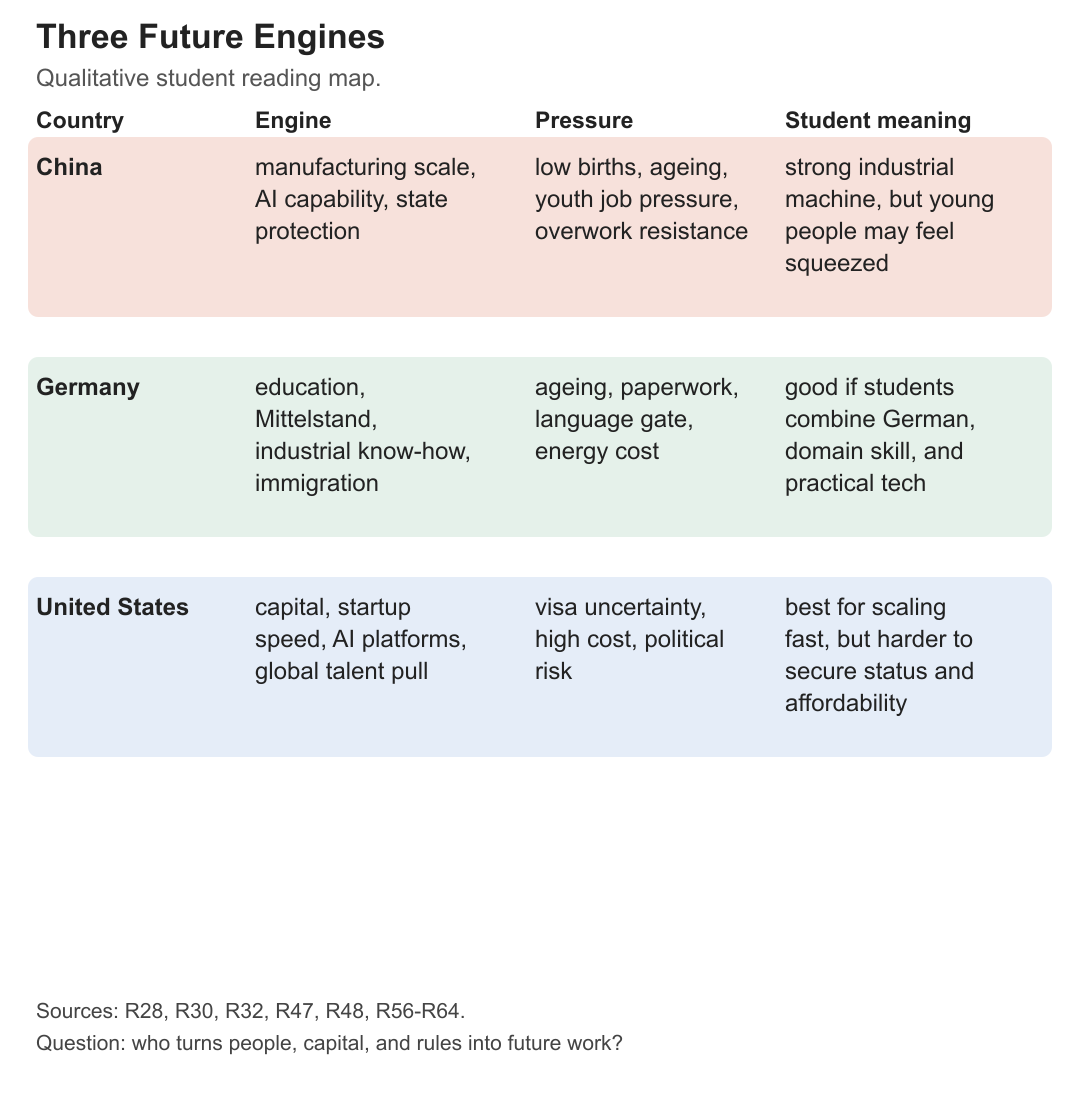

Germany, China, United States: Three Future Engines

So where does Germany stand between China and the United States?

Here is my simple map.

The United States has capital, startup speed, elite AI platforms, and a strong pull for global talent. But immigration status can be painful, healthcare and housing can be expensive, and starting a company does not automatically solve visa life.

China has manufacturing scale, talent, AI ambition, and stronger state protection of strategic companies. But it has low births, ageing, youth unemployment pressure, and less immigration cushion. If the young population feels squeezed, the machine can still be strong while the human mood becomes weaker.

Germany sits in the middle.

Germany does not have US-style AI capital speed. It does not have China-style state control. But it has strong education, applied engineering, Mittelstand know-how, worker institutions, and the ability to import young people through study, Ausbildung, skilled migration, and family migration.

That last point is huge.

China mostly relies on its own population. Germany can renew part of its workforce through immigration. IAB has discussed why Germany needs large annual migration flows to stabilize its labor force [R61]. OECD’s 2025 Germany survey also frames skilled-labor shortage and integration as major policy issues [R62].

But immigration is not magic.

If people arrive but cannot enter good work, cannot learn German fast enough, cannot get credentials recognized, cannot navigate offices, or cannot move from low-wage survival jobs into skilled work, then migration becomes a stress point. If the system works, migration becomes Germany’s advantage.

This is why I want to be careful about welfare and migration discussions.

Some people talk about migrants as if they are only a cost. Some people talk about migration as if every arrival automatically solves Germany’s workforce problem. Both views are too simple.

The real question is:

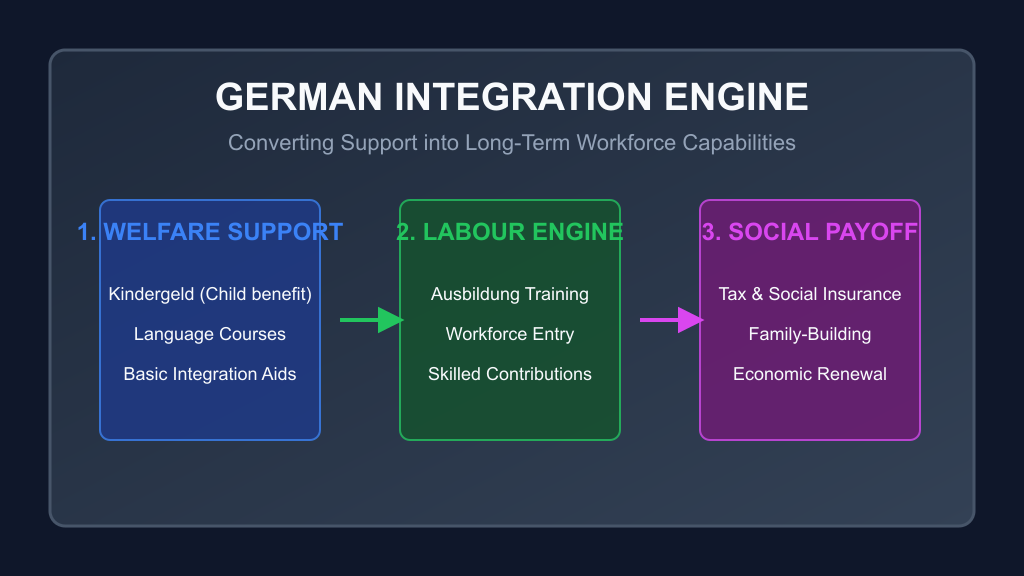

Does Germany convert new people into skilled, working, tax-paying, family-building, company-building people?

Child benefit, welfare support, language courses, Ausbildung support, and integration programs are not automatically bad. They are tools. But if the path does not lead to education and work over time, then the tool becomes expensive and politically fragile.

For Vietnamese readers, this is important. Germany may welcome you as a student, trainee, nurse, IT worker, restaurant worker, or future founder. But the country will not automatically move you upward. You still need German, a useful skill, a network, and a clear understanding of which industries are building future work.

If Germany Loses Equity But Keeps Capability, Is That Still Germany?

This question is the heart of the whole article.

Maybe German people do not own every famous German company in a simple way anymore. Maybe DAX shares are globally held. Maybe some brands have foreign anchor shareholders. Maybe private equity buys suppliers. Maybe Chinese, American, Middle Eastern, and European capital all sit inside the same company story.

So what is still German?

I think there are three levels.

First, there is legal ownership. Who owns the shares? Who has voting rights? Who can sell the company?

Second, there is decision control. Where are board decisions made? Where is R&D budget approved? Where is the next product line decided?

Third, there is capability. Where are the engineers, process experts, factory workers, apprentices, product managers, researchers, and domain experts?

If Germany loses all three, then the brand becomes mostly a memory.

If Germany loses some equity but keeps decision control and capability, the story is still mixed but not dead.

If Germany loses equity and decision control but keeps only old factories, then students should be more careful. That means the future jobs may slowly move away.

This is why I do not want to write a dramatic article saying “Germany is finished.” That is too easy.

The better question is:

Which parts of German capability are still being renewed?

If a company still trains apprentices, invests in R&D in Germany, builds industrial AI in Germany, keeps engineering decisions in Germany, and gives international students a real path into skilled work, then the company is still part of Germany’s future even if some shareholders are foreign.

But if Germany only keeps the logo, the old plant, and the paperwork, then the future is weaker.

What This Means For Students Reading Job Ads

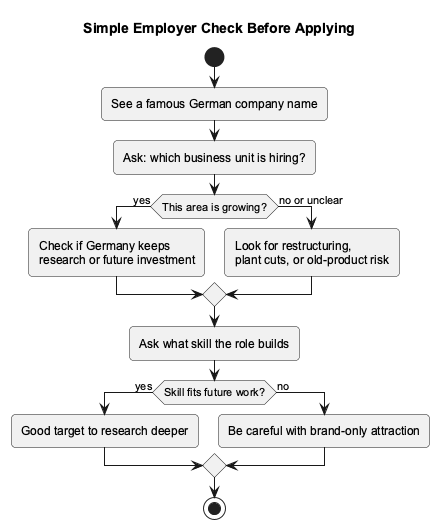

Okay, now the practical part.

If you are a student in Germany, or planning to study here, how should you use this information?

First, do not panic.

Germany still has real companies, real engineering, real training systems, real industrial clusters, and real jobs. The point is not “avoid Germany.” The point is “read the job market with more adult eyes.”

When you see a famous company name, ask:

- Which business unit is hiring?

- Is this area growing or shrinking?

- Is Germany still important for this unit’s future?

- Is research and development here, or only sales/admin?

- Is the company investing in automation, software, energy transition, AI, process improvement, supply-chain resilience, or compliance?

- Is the role close to future work, or only old-product maintenance?

- Is the company cutting jobs in one area while hiring in another?

- Does the company give international students a real path, or only use English words in the career page?

- Does the role build portable skills if Germany’s economy changes?

For Vietnamese readers choosing Germany pathways, I would add a second checklist:

| Path | What to check | Why it matters |

|---|---|---|

| Nursing Ausbildung | German level, shift work, long-term care employer quality, recognition path | Stable demand does not always mean easy work |

| Restaurant or hotel Ausbildung | working hours, pay progression, city, language environment | Entry may be easier, but growth can be limited |

| IT university or master’s route | internship access, German language plan, portfolio, practical projects | Technical skill alone may not bypass language gates |

| Business / Product / Process route | industry knowledge, German workplace language, process tools, stakeholder skills | Good for people who can connect business and technical teams |

| Industrial apprenticeship | company investment, automation exposure, safety, union/works council context | Strong route if linked to future technology, not only old processes |

For IT-background students, I would especially look at roles connected to Germany’s transition problem:

- cloud infrastructure inside German companies

- cybersecurity for industrial systems

- SAP and ERP transformation

- process automation

- AI-assisted operations

- data quality and reporting

- manufacturing software

- logistics and warehouse systems

- healthcare workflow digitization

- energy and grid software

- compliance technology

- AI workflow integration inside normal business departments

These roles sit between old Germany and future Germany.

That is where international students may have a better chance if they combine technical skills with German learning and domain understanding.

If you are deciding whether to stay in Germany, go back to Vietnam, or move somewhere else, I would not make the decision only from salary.

Ask three questions:

- Where can I build skill that stays valuable after AI changes office work?

- Where can I legally and practically move upward, not only survive?

- Where can I understand the language and business culture enough to join the decision layer?

Germany can still be a good answer. But it is not a passive answer. You cannot just arrive, get a certificate, and expect the system to carry you.

You need to choose the right room in the German house.

For me, that means I would focus on IT plus business process, AI-assisted operations, German language, and industries where Germany still has real domain depth: manufacturing, healthcare, logistics, energy, compliance, ERP, cybersecurity, and industrial data.

Here is the simple student check:

For example, “automotive” is not one thing.

A role in old combustion-engine supplier work may have a different risk profile from a role in battery systems, charging software, process automation, procurement risk, cybersecurity, production data, or AI-supported quality control.

Same company. Different future.

My Business Analyst Way Of Looking At This

Maybe this is because of my background in Product Owner and Business Analyst work, but I keep seeing companies as workflows.

A company is not only a logo.

It is a system:

- customers place orders

- suppliers provide parts

- workers create value

- managers make tradeoffs

- investors provide capital

- governments set rules

- students enter as future labor

If one part changes, the whole workflow changes.

For a Business Analyst, the most useful question is often not “Who is good?” or “Who is bad?”

The useful question is:

Who decides what happens next?

In a normal product project, if you do not know who decides, your requirements become messy. In a company ownership story, if you do not know who decides, your job-market understanding also becomes messy.

Failure-Cost Ledger: What Germany Could Lose

Let’s be honest. Foreign ownership is not automatically a failure. But if Germany keeps the brand while losing too much future control, there are costs.

| Risk | What it means in simple words | Who feels it first | Student impact |

|---|---|---|---|

| Research moves away | Future engineering happens elsewhere | engineers, universities, suppliers | fewer advanced roles |

| Factory stays but does not upgrade | Jobs exist today but future products go elsewhere | production workers | fewer trainee and entry jobs |

| Mittelstand succession fails | family owner sells or closes | small towns, suppliers | local job options shrink |

| Supplier margins collapse | parts makers cut cost first | automotive regions | internships and junior roles reduce |

| Brand stays but control moves | logo remains, decisions shift | workers and managers | harder to judge stability |

This is why “jobs saved today” and “future control protected” are not always the same thing.

If an outside investor keeps a factory open for five years, that can be good for families right now. But if the next generation of technology, software, and research moves away, then students may not see the long-term benefit.

The hard question is not “foreign money yes or no?”

The hard question is “what kind of deal protects local future work?”

So, Is Germany Being Bought?

My honest answer: not in the simple dramatic way people say online.

Germany is not one shop with one owner.

It is a huge economy with listed companies, family companies, private companies, public investors, German families, US asset managers, European institutions, Chinese strategic buyers, private equity funds, banks, pension funds, and government rules.

So if someone says “China owns Germany,” I would be careful.

If someone says “foreign ownership does not matter,” I would also be careful.

Both are too simple.

The better sentence is:

Parts of German industry are becoming more dependent on global capital, and that changes who has influence over future decisions.

That sentence is less viral, but more useful.

What I Would Do Differently When Applying In Germany

If I were reading job ads with this article in mind, I would not only ask:

“Is this a famous company?”

I would ask:

“Is this role near the future of the company?”

For my own background, I would look more carefully at roles connected to:

- process improvement

- requirements and workflow design

- automation

- AI-assisted operations

- supply-chain resilience

- quality and compliance

- product transition

- digital tools inside traditional industries

- customer and supplier workflow redesign

Why?

Because when companies are under pressure, they still need people who can make messy work clearer. They need people who can map processes, reduce waste, improve tools, connect business and technical teams, and help old organizations change without collapsing.

This is not only a software story.

It is also a workflow story.

And for students, this may be the opportunity hidden inside the scary headlines.

FAQ

Is foreign ownership bad?

Q1: Is foreign ownership bad?

Not automatically. Foreign ownership can bring money, technology, market access, and survival. The risk is not the passport of the investor. The risk is losing future decision power, research capability, and long-term local investment without noticing it.

Are Mittelstand companies still German?

Q2: Are Mittelstand companies still German?

Many are still German-owned, family-owned, or locally rooted. But they are not protected from pressure. Energy cost, succession, digitalization, export weakness, and customer pressure can still make them vulnerable.

Is China buying Germany?

Q3: Is China buying Germany?

That sentence is too simple. Some Chinese companies have bought or invested in important European industrial assets, and some cases are strategically important. But Germany’s ownership structure also includes US investors, European investors, German families, institutional funds, and normal stock-market ownership. The better question is case by case: what was bought, why, and what decisions moved?

Should students avoid automotive?

Q4: Should students avoid automotive?

Not automatically. Automotive is under pressure, especially old combustion-engine supply chains. But it also has future areas: software, battery systems, charging, automation, procurement, data, cybersecurity, quality systems, and production transformation. You need to look at the specific role and business unit.

Is Germany still a good place to build a career?

Q5: Is Germany still a good place to build a career?

I think yes, but not with lazy assumptions. The old image of “join a famous German company and everything is stable” is weaker now. A better strategy is to understand the company’s future direction, not only its history.

References

[R1] EY. (2025, August 14). Wem gehört der DAX? 2025. https://www.ey.com/de_de/newsroom/2025/08/ey-wem-gehoert-der-dax-2025

[R2] Institut für Mittelstandsforschung Bonn. (2025). Macro-economic significance of SMEs: Germany. https://www.ifm-bonn.org/en/statistics/overview-mittelstand/macro-economic-significance-of-smes/deutschland

[R3] KfW Research. (2025). KfW-Mittelstandspanel 2025. https://www.kfw.de/PDF/Download-Center/Konzernthemen/Research/PDF-Dokumente-KfW-Mittelstandspanel/KfW-Mittelstandspanel-2025.pdf

[R4] Deutsche Bundesbank. (2026). Germany’s external assets in the light of geoeconomic tensions. https://publikationen.bundesbank.de/publikationen-en/reports-studies/monthly-reports/monthly-report-april-2026-993254?article=germany-s-external-assets-in-the-light-of-geoeconomic-tensions-993256

[R5] European Commission. (2024). EU foreign direct investment screening. https://policy.trade.ec.europa.eu/enforcement-and-protection/investment-screening_en

[R6] European Commission. (2025, December 11). Revision of the EU’s Foreign Investment Screening Mechanism. https://policy.trade.ec.europa.eu/news/revision-eus-foreign-investment-screening-mechanism-2025-12-11_en

[R7] KUKA. (2017). KUKA annual report 2016. https://www.kuka.com/-/media/kuka-corporate/documents/ir/reports-and-presentations/en/annual-report/kuka-annual-report-2016.pdf?hash=CF6BBC70885A83F5D4CF9EADCEBEEB81&rev=c976cc2263ef434682a6dbe81fd3e25f

[R8] PR Newswire. (2010, August 2). Geely Holding Group completes acquisition of Volvo Car Corporation. https://www.prnewswire.com/news-releases/geely-holding-group-completes-acquisition-of-volvo-car-corporation-99745519.html

[R9] Pirelli. (2015, March 31). Pirelli board retains Deutsche Bank and Goldman Sachs as advisors for the consideration of the announced Camfin-ChemChina tender offer. https://press.pirelli.com/pirelli-board-retains-deutsche-bank-and-goldman-sachs-as-advisors-for-the-consideration-of-the-announced-camfin-chemchina-tender-offer/

[R10] Eurofound. (2024). Ebro: Business expansion in Spain. https://apps.eurofound.europa.eu/restructuring-events/detail/201570

[R11] Google DeepMind. (2026). Get started with image generation with Gemini 3 Pro Image. https://deepmind.google/models/gemini-image/prompt-guide/

[R12] Google. (2025, August 26). Nano Banana: Image editing in Google Gemini gets a major upgrade. https://blog.google/products-and-platforms/products/gemini/updated-image-editing-model/

[R14] Mercedes-Benz Group. (2026). Shareholder structure. https://group.mercedes-benz.com/investors/share/shareholder-structure/

[R15] BMW Group. (2026). BMW Group stock shares. https://www.bmwgroup.com/en/investor-relations/bmw-shares.html?ntvDuo=true

[R16] Volkswagen Group. (2026). Shareholder structure. https://www.volkswagen-group.com/en/shareholder-structure-15951

[R17] Porsche AG. (2026). The share. https://investorrelations.porsche.com/en/the-share

[R18] Bosch. (2026). Company. https://www.bosch.com/company/

[R19] SAP. (2026). Aktionärsstruktur & Basisdaten. https://www.sap.com/investors/de/stock/basic-data.html

[R20] Siemens. (2026). Aktionärsstruktur und Stimmrechtsmitteilungen. https://www.siemens.com/de-de/company/investor-relations/share-bonds-rating/shareholder-structure-voting-rights-announcements/

[R21] Deutsche Telekom. (2026). Shareholder structure. https://www.telekom.com/en/investor-relations/share/shareholder-structure

[R22] Allianz. (2026). Shareholder structure. https://www.allianz.com/en/investor_relations/share/shareholder-structure.html

[R23] BASF. (2026). Shareholder structure. https://www.basf.com/global/en/investors/share-and-adrs/shareholder-structure

[R24] adidas. (2026). Our Share – adidas Annual Report 2025. https://report.adidas-group.com/2025/en/to-our-shareholders/our-share.html

[R25] Schwarz Digits. (2026). Digital sovereignty for Europe. https://schwarz-digits.de/

[R26] ALDI US. (2026). Corporate inquiries. https://www.aldi.us/about-aldi/faqs/corporate-inquiries

[R28] Statistisches Bundesamt. (2026). Foreign population by sex and selected citizenships. https://www.destatis.de/EN/Themes/Society-Environment/Population/Migration-Integration/Tables/foreigner-gender.html

[R29] Statistisches Bundesamt. (2026). Foreign population by place of birth. https://www.destatis.de/EN/Themes/Society-Environment/Population/Migration-Integration/Tables/foreigner-place-of-birth.html

[R30] Statistisches Bundesamt. (2025). Migration. https://www.destatis.de/DE/Themen/Gesellschaft-Umwelt/Bevoelkerung/Wanderungen/_inhalt.html?templateQueryString=Migration

[R31] Statistisches Bundesamt. (2025). Naturalisations, 2000 to 2024. https://www.destatis.de/EN/Themes/Society-Environment/Population/Migration-Integration/Tables/naturalisations-rate.html

[R32] German Academic Exchange Service. (2024, December 19). Number of international students in Germany expected to rise to over 400,000. https://www.daad.de/en/press-releases/2024/zahl-internationaler-studierender-in-deutschland-steigt-auf-ueber-400000/

[R33] Bundesagentur für Arbeit. (2026). Auszubildende aus dem Ausland. https://www.arbeitsagentur.de/vor-ort/zav/presse/2026-2-auszubildende-aus-dem-ausland

[R35] TechCrunch. (2026, April 27). China blocks Meta’s $2B Manus deal after months-long probe. https://techcrunch.com/2026/04/27/china-vetoes-metas-2b-manus-deal-after-months-long-probe/

[R37] UNCTAD Investment Policy Hub. (2021). China: Foreign Investment Security Review Measures. https://investmentpolicy.unctad.org/investment-laws/laws/570/foreign-investment-security-review-measures

[R38] State Council of the People’s Republic of China. (2024, September 8). China to lift foreign investment access restrictions in manufacturing sector. https://english.www.gov.cn/news/202409/08/content_WS66dd6238c6d0868f4e8eabad.html?os=f

[R39] State Council of the People’s Republic of China. (2024, June 19). China to facilitate foreign investors investing in domestic securities: official. https://english.www.gov.cn/news/202406/19/content_WS6672cbb5c6d0868f4e8e8546.html

[R40] Center for Security and Emerging Technology. (2023). Chinese Catalogue of Technologies Prohibited or Restricted from Export. https://cset.georgetown.edu/publication/china-export-control-catalog-2023/

[R41] KfW Research. (2025). KfW Entrepreneurship Monitor 2025. https://www.kfw.de/PDF/Download-Center/Konzernthemen/Research/PDF-Dokumente-Gr%C3%BCndungsmonitor/Gr%C3%BCndungsmonitor-englische-Dateien/KfW-Gr%C3%BCndungsmonitor-2025_EN.pdf

[R42] Federal Ministry for Economic Affairs and Climate Action. (2026). EXIST: From science to business. https://exist.de/

[R43] Existenzgründungsportal. (2026). Business in Germany. https://www.existenzgruendungsportal.de/Navigation/EN/Home/home

[R44] OECD. (2025). Inclusive entrepreneurship policy country assessment notes: Germany. https://www.oecd.org/content/dam/oecd/en/publications/reports/2025/05/inclusive-entrepreneurship-policy-assessment-country-notes_48c462fc/germany_8a7417f9/dc03aa55-en.pdf

[R45] Startup Verband. (2025). Deutscher Startup Monitor 2025. https://startupverband.de/fileadmin/startupverband/mediaarchiv/research/dsm/Deutscher_Startup_Monitor_2025.pdf

[R46] Delaware Division of Corporations. (2026). Service of process and fee schedule. https://corp.delaware.gov/fee/

[R47] Stripe Atlas. (2026). Incorporate your company. https://stripe.com/de/atlas

[R48] U.S. Small Business Administration. (2026). Choose a business structure. https://www.sba.gov/business-guide/launch-your-business/choose-business-structure

[R49] State Council of the People’s Republic of China. (2026). Do business in China. https://english.www.gov.cn/services/doingbusiness/

[R50] Ministry of Commerce of the People’s Republic of China. (2026). Enterprise registration. https://fdi.mofcom.gov.cn/EN/come-newzonghe.html?comeID=5&name=Enterprise+Registration&parentId=126

[R51] Federal Office for the Safety of Nuclear Waste Management. (2023). Nuclear phase-out. https://www.base.bund.de/en/nuclear-safety/nuclear-phase-out/nuclear-phase-out_content.html

[R52] U.S. Energy Information Administration. (2023, February 16). Germany extends the lifetime of all three remaining nuclear plants. https://www.eia.gov/todayinenergy/detail.php?id=55559

[R53] Fraunhofer Institute for Solar Energy Systems ISE. (2024, April 15). Status quo one year since Germany’s nuclear exit. https://www.ise.fraunhofer.de/en/press-media/press-releases/2024/status-quo-one-year-since-germanys-nuclear-exit-renewable-capacity-expands-electricity-from-fossil-fuels-significantly-reduced.html

[R54] International Energy Agency. (2025). Germany 2025. https://www.iea.org/reports/germany-2025

[R55] Agora Energiewende. (2025). State of the energy transition in Germany: Annual review 2025. https://www.agora-energiewende.org/publications/state-of-the-energy-transition-in-germany-annual-review-2025

[R56] National Bureau of Statistics of China. (2025, January 17). Statistical Communiqué of the People’s Republic of China on the 2024 National Economic and Social Development. https://www.stats.gov.cn/english/PressRelease/202501/t20250117_1958330.html

[R57] Reuters via TradingView. (2025, September 17). China’s youth jobless rate climbs to 18.9% in August. https://www.tradingview.com/news/reuters.com%2C2025%3Anewsml_P8N3UL0FK%3A0-china-s-youth-jobless-rate-climbs-to-18-9-in-august/

[R58] World Youth Development Forum. (2026). Facts & Figures of Global Youth Development. https://www.wydf.org.cn/zh/knowledge_base/youth_publication/202507/W020260109594764617375.pdf

[R59] Ren, X., Abdullah, H., Shaffril, H. A. M., Rahman, H. A., & Zaremohzzabieh, Z. (2026). A scoping review of “Tang ping” (Lying flat) and mental health status among Chinese youth. PLOS ONE. https://journals.plos.org/plosone/article?id=10.1371/journal.pone.0342591

[R60] Stanford Institute for Human-Centered Artificial Intelligence. (2026). The 2026 AI Index Report. https://hai.stanford.edu/ai-index/2026-ai-index-report

[R61] Institut für Arbeitsmarkt- und Berufsforschung. (2023, April 17). Warum braucht Deutschland 400.000 Migrantinnen und Migranten pro Jahr? https://iab.de/warum-braucht-deutschland-400-000-migrantinnen-und-migranten-pro-jahr/

[R62] OECD. (2025). Addressing skilled labour shortages: OECD Economic Surveys: Germany 2025. https://www.oecd.org/en/publications/2025/06/oecd-economic-surveys-germany-2025_b395dc9b/full-report/addressing-skilled-labour-shortages_9edb78e6.html

[R64] China Briefing. (2021, September 6). “996” is Ruled Illegal: Understanding China’s Changing Labor System. https://www.china-briefing.com/news/996-is-ruled-illegal-understanding-chinas-changing-labor-system/

Related Reading

- https://pmlecuong.com/drawing-the-line-how-diagrams-and-ai-save-product-teams-in-2025/

- https://pmlecuong.com/agents-are-just-tools-in-a-loop-and-thats-why-they-work/

- https://pmlecuong.com/context-engineering-vs-vibe-coding-a-business-persons-technical-discovery-part-1-of-2/